UAE Financial License Strategy: Three Questions Every Founder Must Answer First

Most UAE licensing conversations start with the wrong question.

Founders ask which license is fastest. Which jurisdiction costs less. Which regulator sounds more prestigious. Which setup can be completed with the least friction.

Those are understandable questions, but they are not the questions that determine whether a UAE financial license is right for the business.

In regulated financial services, the license is not just an operating permission. It becomes part of the company’s commercial identity, investor narrative, compliance burden, market access, and long-term structure.

Choose correctly, and the license becomes a strategic asset.

Choose poorly, and the license becomes a constraint that may limit your market, delay partnerships, complicate fundraising, or force a restructuring later.

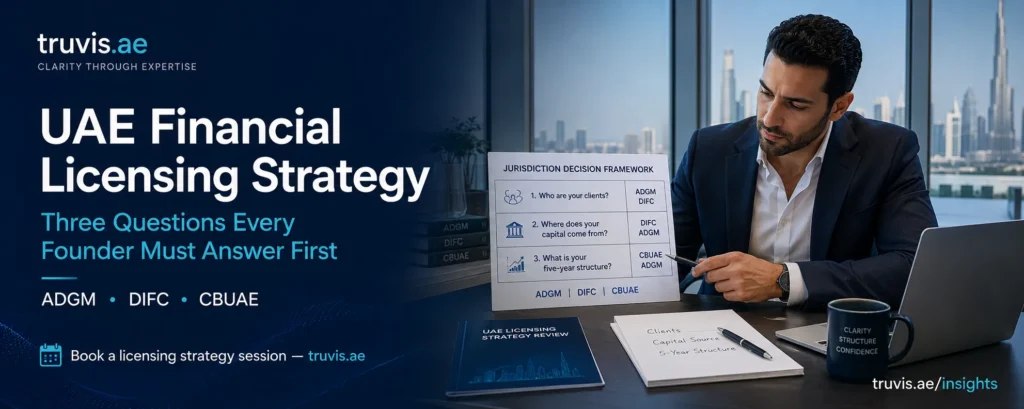

For fintech founders, investment firms, payment businesses, digital asset companies, and financial institutions entering the UAE, the licensing decision should begin with three questions:

- Who are your clients?

- Where does your capital come from?

- What is your five-year structure?

If these three questions are not answered clearly, the jurisdiction decision is not ready.

Why speed, cost, and prestige are the wrong first filters

Speed matters. Cost matters. Reputation matters.

But none of them should be the first filter in UAE financial licensing.

A fast license in the wrong jurisdiction is not efficient. It is expensive later.

A lower-cost structure that cannot serve the intended customer base is not economical. It is misaligned.

A prestigious license that does not match the company’s commercial model is not strategic. It is cosmetic.

This is where many founders get the UAE wrong. They approach licensing as an administrative process, when it should be treated as a strategic design decision.

The UAE does not operate through one unified financial regulatory system. It has three major financial regulatory environments: DIFC with the DFSA, ADGM with the FSRA, and the CBUAE onshore framework. Each serves a different market, with different legal systems, regulatory expectations, licensing categories, and commercial use cases.

That is why the right question is not:

“Which license is best?”

The right question is:

“Which licensing framework matches the business we are actually building?”

1. Who are your clients?

The first licensing question is always the client question.

Who will the business serve?

Retail UAE consumers? SMEs? Banks? Asset managers? Professional investors? Family offices? International institutions? Merchants? Payment users? Crypto-native clients? Government-linked entities?

The answer determines the regulatory perimeter.

If the business is serving retail consumers across the UAE, the CBUAE framework becomes highly relevant. A consumer-facing payments app, digital wallet, open finance platform, BNPL model, retail insurance intermediary, or mass-market financial product generally cannot rely on a financial free zone license alone to serve the full UAE market.

DIFC and ADGM are powerful jurisdictions, but they are financial free zones. Their licenses do not automatically authorise unrestricted retail activity across the UAE mainland.

This is one of the most common founder mistakes.

A fintech founder may choose ADGM or DIFC because the jurisdiction sounds familiar to investors. Later, the founder discovers that the product needs access to UAE retail customers, banking integrations, or consumer financial activity that sits under the CBUAE framework.

At that point, the company may need a second licensing pathway, a revised business model, or a full restructuring.

The client question avoids this.

If your clients are retail UAE consumers

The CBUAE pathway should be assessed early.

This applies especially to:

- Payment services

- Open finance providers

- Account information services

- Payment initiation services

- Digital wallets

- Consumer lending models

- BNPL or credit products

- Retail insurance or financial distribution models

- Consumer-facing fintech platforms

The reason is simple. Retail market access is regulated differently from institutional or cross-border activity.

If your clients are institutions or professional counterparties

DIFC or ADGM may be more appropriate.

This applies to:

- Investment management

- Fund structures

- Advisory firms

- Institutional fintech

- Wealth management platforms

- Capital markets activity

- Financial infrastructure serving professional clients

- Family office or private investment structures

Here, the value of DIFC or ADGM is not just the license. It is the legal architecture, regulatory credibility, common law environment, and institutional ecosystem.

If your clients are international

The analysis becomes more nuanced.

A UAE-based company serving non-UAE clients may not need the same licensing path as a company targeting UAE retail consumers. But the regulated activity still matters. Cross-border activity, financial promotion, client location, onboarding process, and product type all need to be mapped.

This is why client type must come first.

Before asking “ADGM or DIFC?”, ask “Who exactly are we allowed to serve?”

2. Where does your capital come from?

The second question is the capital question.

A licensing strategy is not only about customers. It is also about investors, lenders, partners, and institutional relationships.

Where does the capital come from?

Abu Dhabi sovereign ecosystem? Dubai financial institutions? International venture capital? Regional family offices? Global asset managers? Strategic banking partners? Private wealth networks?

The answer can change the licensing recommendation.

When ADGM has a natural advantage

ADGM has strong alignment with Abu Dhabi’s sovereign, institutional, and innovation ecosystem.

For founders whose capital strategy involves Abu Dhabi-linked investors, sovereign wealth relationships, government-backed innovation programmes, asset management, digital assets, or financial infrastructure, ADGM can provide strategic proximity.

That proximity is not only geographic. It is reputational and ecosystem-based.

ADGM is often relevant for:

- Fintech founders seeking FSRA pathways

- Digital asset firms

- Fund managers

- Asset management platforms

- Innovation-led financial businesses

- Sovereign-connected capital strategies

- Abu Dhabi-based institutional relationships

If the company’s five-year funding story depends on Abu Dhabi relationships, ADGM may be more than a licensing choice. It may be part of the capital strategy.

When DIFC has a natural advantage

DIFC has a deeply established Dubai financial ecosystem.

It is often relevant for companies whose capital, clients, or partners are connected to Dubai’s institutional market, global banks, asset managers, law firms, consulting firms, fund platforms, and international corporate networks.

DIFC is often relevant for:

- Global financial institutions

- Fund managers

- Wealth and advisory firms

- Institutional fintech platforms

- Capital markets firms

- Trade finance businesses

- Insurance and reinsurance structures

- Dubai-facing financial services companies

If the business needs a globally recognised financial centre address in Dubai, DIFC may support the commercial story better.

When CBUAE alignment matters

CBUAE licensing is not chosen for prestige positioning. It is chosen because the business model requires onshore UAE market access.

For payment businesses, Open Finance providers, retail fintechs, or other consumer-facing financial services, CBUAE authorisation may be the core licensing requirement.

In these cases, capital providers will ask a direct question:

Can this business legally serve the market it claims to serve?

If the answer depends on CBUAE licensing, investors will expect that pathway to be understood before serious fundraising.

3. What is your five-year structure?

The third question is the structure question.

Where does the business need to be in five years?

This is the question founders often skip.

They focus on the first license, first launch, first bank account, first investor meeting, or first product release. But regulatory structure is path-dependent. The jurisdiction chosen today can shape what is easy, difficult, expensive, or impossible later.

A founder should not choose a license only for year one.

They should ask:

- Will this company remain a single UAE entity?

- Will it need both free zone and onshore permissions?

- Will it raise institutional capital?

- Will it expand into Saudi Arabia or the wider GCC?

- Will it serve retail users or professional clients?

- Will it need a holding company?

- Will it need regulated subsidiaries?

- Will it need to separate technology IP from regulated activity?

- Will it eventually need CBUAE authorisation after proving the model in ADGM or DIFC?

The answer determines sequencing.

Example: fintech testing before full authorisation

An early-stage fintech may not be ready for a full regulatory license. It may need to test the product, prove demand, refine compliance controls, and build regulator confidence first.

In that case, a sandbox or innovation pathway may be more appropriate than jumping directly into a full license.

Example: institutional first, retail later

Some founders begin with institutional clients and later expand into retail consumers.

That may support a phased structure:

First, DIFC or ADGM for institutional credibility.

Later, CBUAE licensing if the business enters the UAE retail market.

This is not duplication. It is strategic sequencing.

Example: technology provider vs regulated provider

Some businesses describe themselves as fintech companies but are actually technology vendors to regulated institutions.

Others are directly performing regulated activities.

The five-year structure question helps identify whether the company should remain a software provider, become a regulated provider, or operate through a group structure where technology, IP, and regulated activity are separated.

This distinction matters for licensing, tax, governance, banking, and investor diligence.

How the answers map to jurisdictions

There is no universal best jurisdiction for UAE financial license services.

There is only the best fit for a specific business model.

Here is the practical decision framework.

CBUAE

CBUAE is generally the strongest fit when the company needs direct UAE onshore market access.

Best suited for:

- Retail payment services

- Open finance providers

- Consumer-facing fintech

- Digital wallets

- UAE retail banking integration

- Payment initiation

- Account information services

- Consumer finance models

- Financial products serving UAE residents at scale

Strategic value:

- Full UAE market reach

- Direct relevance to retail financial activity

- Strong regulatory credibility for consumer-facing models

- Necessary pathway where the activity falls under Central Bank supervision

Key consideration:

The CBUAE pathway usually requires stronger operational, governance, compliance, and capital readiness. It should not be treated as a basic company formation route.

ADGM

ADGM is generally the strongest fit when the business needs Abu Dhabi ecosystem alignment, institutional legal architecture, innovation pathways, or FSRA-regulated financial activity.

Best suited for:

- Fintech innovation

- Digital assets

- Asset management

- Fund structures

- Institutional financial services

- Sovereign-connected capital strategies

- RegLab or staged regulatory pathways

- Abu Dhabi-based strategic growth

Strategic value:

- English common law framework

- Strong FSRA regulatory architecture

- Abu Dhabi capital ecosystem proximity

- Innovation-friendly regulatory environment

- Strong fit for structured financial businesses and emerging financial technology

Key consideration:

ADGM is not a shortcut to unrestricted UAE retail access. If the model depends on UAE consumers nationwide, CBUAE analysis may still be required.

DIFC

DIFC is generally the strongest fit when the business needs Dubai-based financial centre credibility, global institutional recognition, or DFSA-regulated activity.

Best suited for:

- Asset managers

- Advisory firms

- Wealth platforms

- Institutional fintech

- Insurance and reinsurance

- Capital markets activity

- Trade finance

- Dubai-facing financial institutions

- International financial firms entering the region

Strategic value:

- Mature financial ecosystem

- Global institutional recognition

- DFSA regulatory credibility

- Strong professional services network

- Dubai commercial proximity

Key consideration:

DIFC is highly credible, but credibility alone is not enough. The license must match the customer base and activity.

Common mistakes when the three questions are skipped

When founders skip the client, capital, and five-year structure questions, the same mistakes appear repeatedly.

Mistake 1: Choosing based on prestige

A founder chooses DIFC or ADGM because the name sounds strong in investor conversations.

The problem appears later when the business model requires CBUAE authorisation.

Prestige does not replace regulatory fit.

Mistake 2: Choosing based on cost

A founder selects the lower-cost route without mapping activity scope, capital expectations, governance requirements, or market access.

The structure looks efficient at the start but becomes expensive when the business needs to upgrade, restructure, or apply again elsewhere.

Mistake 3: Choosing based on speed

Fast licensing can be useful only when the license is correct.

If the license does not allow the business to operate as intended, speed has no strategic value.

Mistake 4: Ignoring investor diligence

Investors will not only ask whether the company is licensed.

They will ask whether the license matches the product, market, revenue model, and regulatory risk.

A weak licensing rationale can damage investor confidence even if the company has an impressive product.

Mistake 5: Treating the license as a one-time event

Financial licensing is not finished at approval.

It creates ongoing obligations around governance, compliance, reporting, capital adequacy, senior management, AML and CFT controls, risk management, outsourcing, data protection, and regulator engagement.

A founder who is not prepared for post-license obligations is not ready for licensing.

The strategic takeaway

The UAE offers one of the most sophisticated financial regulatory environments in the region.

That is an advantage for serious founders.

But sophistication also means the licensing decision cannot be made casually.

Before selecting ADGM, DIFC, or CBUAE, founders should answer three questions with precision:

- Who are your clients?

- Where does your capital come from?

- What is your five-year structure?

These questions reveal the real licensing path.

They show whether the business needs onshore authorisation, financial centre credibility, innovation-stage testing, institutional positioning, or a phased regulatory architecture.

They also prevent the most expensive mistake in UAE financial licensing:

Choosing a license before understanding the business model.

Book a licensing strategy session

TruVis advises founders, fintech companies, financial institutions, and investment firms on UAE licensing strategy across ADGM, DIFC, and CBUAE pathways.

If you are evaluating a UAE financial license, do not start with the application.

Start with the strategy.

Book a UAE financial license strategy session at truvis.ae

Related TruVis services

- Banking and treasury support — corporate account opening and banking relationships.

- Uae company formation — mainland, free zone and ADGM setup, end to end.