DIFC vs ADGM vs CBUAE: The Definitive Guide for Financial Institutions Entering the UAE

The most consequential decision a financial institution or fintech company makes when entering the UAE market is rarely the one they spend the most time on.

It is not the product roadmap, the commercial partnerships, or the go-to-market strategy. It is the jurisdiction decision: where, and under whose regulatory oversight, the company will be licensed.

Get this right and the regulatory framework becomes a strategic asset. Get it wrong and it becomes an expensive constraint that may require a costly restructuring years later, when the company is larger, more complex, and considerably less agile.

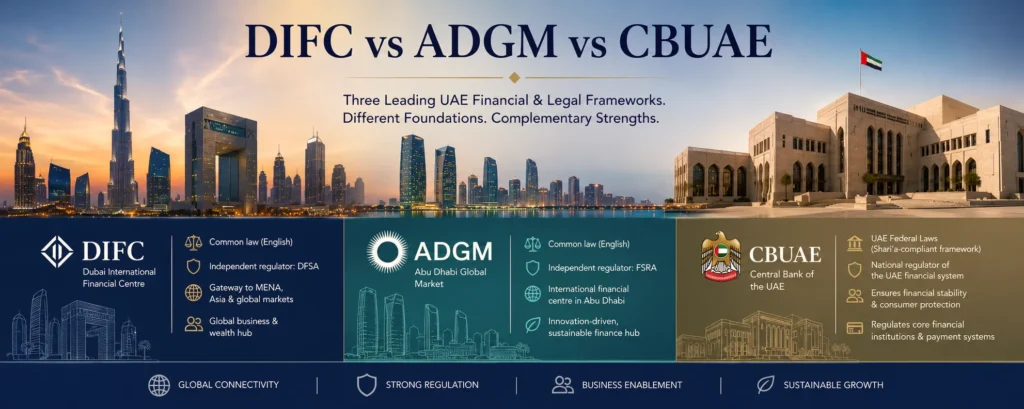

The UAE operates under three distinct and largely independent regulatory frameworks: the Dubai International Financial Centre (DIFC), the Abu Dhabi Global Market (ADGM), and the Central Bank of the UAE (CBUAE). Each serves different markets, operates under different legal systems, and offers different strategic advantages. None of them recognise each other’s licences.

Most founders only discover this distinction two years in. This guide ensures you do not make that mistake.

| 4,000+ Companies in DIFC | 2016 ADGM RegLab Founded | 7 Emirates CBUAE Full Market Reach | 0% CT on Qualifying DIFC/ADGM Income |

DIFC – Dubai International Financial Centre

DIFC is the UAE’s largest and most internationally prominent financial free zone, established under its own civil and commercial laws, independent courts, and a regulatory system entirely separate from the wider UAE legal framework. Regulated by the Dubai Financial Services Authority (DFSA), DIFC is home to over 4,000 companies including more than 1,000 regulated financial services firms.

The DFSA’s regulatory standards are closely aligned with those of the UK Financial Conduct Authority, providing significant familiarity and comfort for international firms with existing European regulatory experience. The DIFC Innovation Hub has attracted over 500 fintech and technology companies, and the FinTech Hive accelerator connects startups directly with major financial institutions for pilot programmes and commercial partnerships.

In 2022, the DFSA introduced a comprehensive Crypto Token Regime, one of the region’s most detailed regulatory frameworks for digital assets, covering investment token services, crypto token services, and custody. In early 2025, the DFSA formally recognised USDC and EURC under this regime.

DFSA Licence Categories

| Category | Activity | Base Capital | Typical Entity |

| Cat 1 | Banking and Deposit-Taking | USD 10M+ | Full-service and digital banks |

| Cat 2 | Dealing as Principal | USD 2M+ | Broker-dealers, market makers |

| Cat 3A | Dealing (Agency and Matched) | USD 500K | STP brokers, execution platforms |

| Cat 3C | Fund Management | USD 140K+ | Asset managers, family offices |

| Cat 3D | Payment Services | USD 500K+ | Payment platforms, PSPs, e-wallets |

| Cat 4 | Advisory and Arranging | USD 10K+ | Advisory firms, fintech arrangers |

DIFC is particularly well-suited for: international banks establishing a regional hub, global asset managers serving MENA institutional investors, fintech companies targeting institutional clients, capital markets and corporate finance firms, family offices and wealth platforms, and digital asset firms requiring globally recognised regulatory credentials.

ADGM – Abu Dhabi Global Market

The Abu Dhabi Global Market (ADGM) is Abu Dhabi’s international financial centre, established on Al Maryah Island as an independent jurisdiction with its own English common law system, courts, and the Financial Services Regulatory Authority (FSRA). ADGM’s strategic positioning reflects Abu Dhabi’s role as a capital of sovereign wealth and long-term institutional investment. As of 2026, ADGM’s jurisdiction has expanded to encompass Al Reem Island, significantly extending its commercial footprint.

ADGM’s ecosystem centres on Abu Dhabi’s sovereign wealth universe. ADIA, Mubadala, and ADQ are its institutional neighbours. But ADGM’s most significant differentiation is its fintech innovation infrastructure. The ADGM RegLab, launched in 2016, was the first regulatory sandbox in the MENA region. Its structured pathway from sandbox participation to full Financial Services Permission has become a proven route to regulatory authorisation.

ADGM pioneered the region’s virtual assets framework in 2018 and in 2021 introduced the first Third Party Provider (TPP) regulatory framework in MENA, creating the regulatory foundation for Open Banking and Open Finance services. In 2025, proposed rules for virtual asset staking were published for consultation, with over 20 regulated firms now conducting virtual asset activities within ADGM.

ADGM Innovation Ecosystem

| RegLab | First regulatory sandbox in MENA (2016). Typical duration 12-24 months. Proven graduation pathway to full Financial Services Permission. Target: fintech startups with genuine innovation and live-testing readiness. Lean Technologies, the first licensed TPP in MENA, graduated from the RegLab before obtaining its full FSP. |

| Digital Lab | Centralised digital testing environment using synthetic data and simulated core banking environments. API Gateway for building integrations within FSRA secure cloud infrastructure. Enables safe, supervised co-development between fintechs and financial institutions. |

| Hub71 | Abu Dhabi’s global technology ecosystem headquartered within ADGM. Access to venture capital funds, subsidised office space and housing, corporate partners, and government institutions. Cost-effective base for pre-licence build and scale. |

ADGM is particularly well-suited for: sovereign wealth funds and institutional asset managers with Abu Dhabi connections, fintech startups seeking the RegLab pathway, TPP and Open Finance providers, digital asset and virtual asset service providers, fund managers in PE, VC, and hedge funds, and firms seeking a UK-equivalent regulatory environment with Abu Dhabi market access.

CBUAE – Central Bank of the UAE

The Central Bank of the UAE (CBUAE) is the federal financial regulatory authority responsible for banking, payment services, insurance, and the Open Finance ecosystem across the UAE’s onshore territory – everything outside the DIFC and ADGM financial free zones.

This distinction is critical: CBUAE regulation means operating under UAE federal law, which confers the broadest possible market access. Regulated entities can directly serve consumers and businesses across all seven emirates without geographic restrictions. If your business model depends on reaching UAE residents directly in payments, BNPL, digital banking, or retail insurance – CBUAE licensing is not optional. It is the only path.

The CBUAE’s regulatory mandate was significantly expanded by Federal Decree Law No. 6 of 2025, which consolidated regulation of banks, payment providers, and insurers under a single comprehensive framework and explicitly captured Open Finance Services as a Licensed Financial Activity for the first time.

Open Finance Framework (2024) – Why It Matters

The CBUAE’s Open Finance Regulation, published in April 2024, creates a mandatory framework for cross-sectoral sharing of financial data – not just payment accounts, but banking, insurance, and investment products simultaneously. This makes it one of the most comprehensive open finance regimes in the world. Participation is mandatory for all CBUAE-licensed banks. All Open Finance Providers access customer data via a common API Hub operated by Al Etihad Payments. Compliance deadline for entities newly in scope: 16 September 2026.

Principal CBUAE Licence Categories

| Licence | Scope | Typical Entities | Key Capital Requirement |

| Banking Licence | Deposits, credit, full banking services | Commercial and digital banks | Basel III capital adequacy |

| Finance Company Licence | Credit, BNPL, auto finance (no deposits) | BNPL platforms, consumer finance | Risk-based |

| Retail Payment Services (Cat I-IV) | Payment initiation, accounts, stored value, cards | PSPs, e-wallets, gateways | Varies by category |

| Open Finance Provider | Data Sharing and Service Initiation across sectors | Open Finance fintechs, TPPs | AED 1,000,000 minimum |

| Stored Value Facility | Issue and operate e-money and prepaid instruments | E-wallet issuers, prepaid cards | Risk-based |

| Insurance Licence | Underwrite life, non-life, takaful products | Insurance companies, takaful operators | Solvency-based |

CBUAE licensing is essential for: any business requiring direct access to UAE retail consumers, Open Finance and fintech providers needing mandatory API access to all UAE banks, payment service providers serving UAE businesses and consumers, digital banks and neobanks for UAE residents, BNPL and consumer credit platforms, and any entity whose model requires nationwide UAE market distribution.

Side by Side – The Comparison That Decides Everything

| Dimension | DIFC | ADGM |

| Legal system | English common law (independent) | English common law (independent) |

| Regulator | DFSA | FSRA |

| Target market | Institutional, HNW, international | Sovereign, institutional, Abu Dhabi |

| Geographic access | DIFC ecosystem and cross-border | ADGM ecosystem and cross-border |

| Corporate tax | 0% on qualifying income | 0% on qualifying income |

| Innovation pathway | ITL + Innovation Hub + FinTech Hive | RegLab + Digital Lab + Hub71 |

| Digital assets | Comprehensive Crypto Token Regime (2022) | Pioneer MENA framework (2018), most advanced |

| Open Finance | Not primary framework | TPP framework (2021) – first in MENA |

| International recognition | Very high – globally prominent | High and growing rapidly |

| Advisory licence capital | USD 10,000 minimum (Cat 4) | USD 10,000 minimum (Cat 4) |

Related TruVis services

- Banking and treasury support — corporate account opening and banking relationships.

- Corporate representative services — local representation and liaison for your UAE entity.